Strategy’s Stock Falters While Bitcoin Treasury Expands

We may earn commissions from affiliate links or include sponsored content, clearly labeled as such. These partnerships do not influence our editorial independence or the accuracy of our reporting. By continuing to use the site you agree to our terms and conditions and privacy policy.

Strategy Inc. (NASDAQ: MSTR), previously known as MicroStrategy, is facing a sharp contrast between its equity performance and its Bitcoin accumulation strategy.

The company’s shares have weakened across multiple timeframes, even as its Bitcoin yield accelerates, leaving investors debating the true value of holding MSTR as a proxy for crypto exposure. For some, the stock represents an innovative way to tap into Bitcoin’s long-term upside without holding the asset directly. For others, the volatility in equity markets, combined with dilution risks and valuation pressure, makes MSTR a far riskier play than simply buying Bitcoin itself. This split in sentiment highlights how Strategy has become more than just a business software firm, it now embodies the broader debate over whether corporations can successfully act as large-scale Bitcoin treasuries while delivering consistent returns to shareholders.

At the same time, the search for alternatives is leading investors to examine other equity-linked plays in the sector. HYLQ Strategy Corp has emerged in these conversations, gradually earning recognition as one of the top cryptocurrency stocks to watch. Its positioning as a regulated gateway into DeFi adds a new dimension to the evolving landscape of crypto-related equities.

Stock slides despite broader market gains

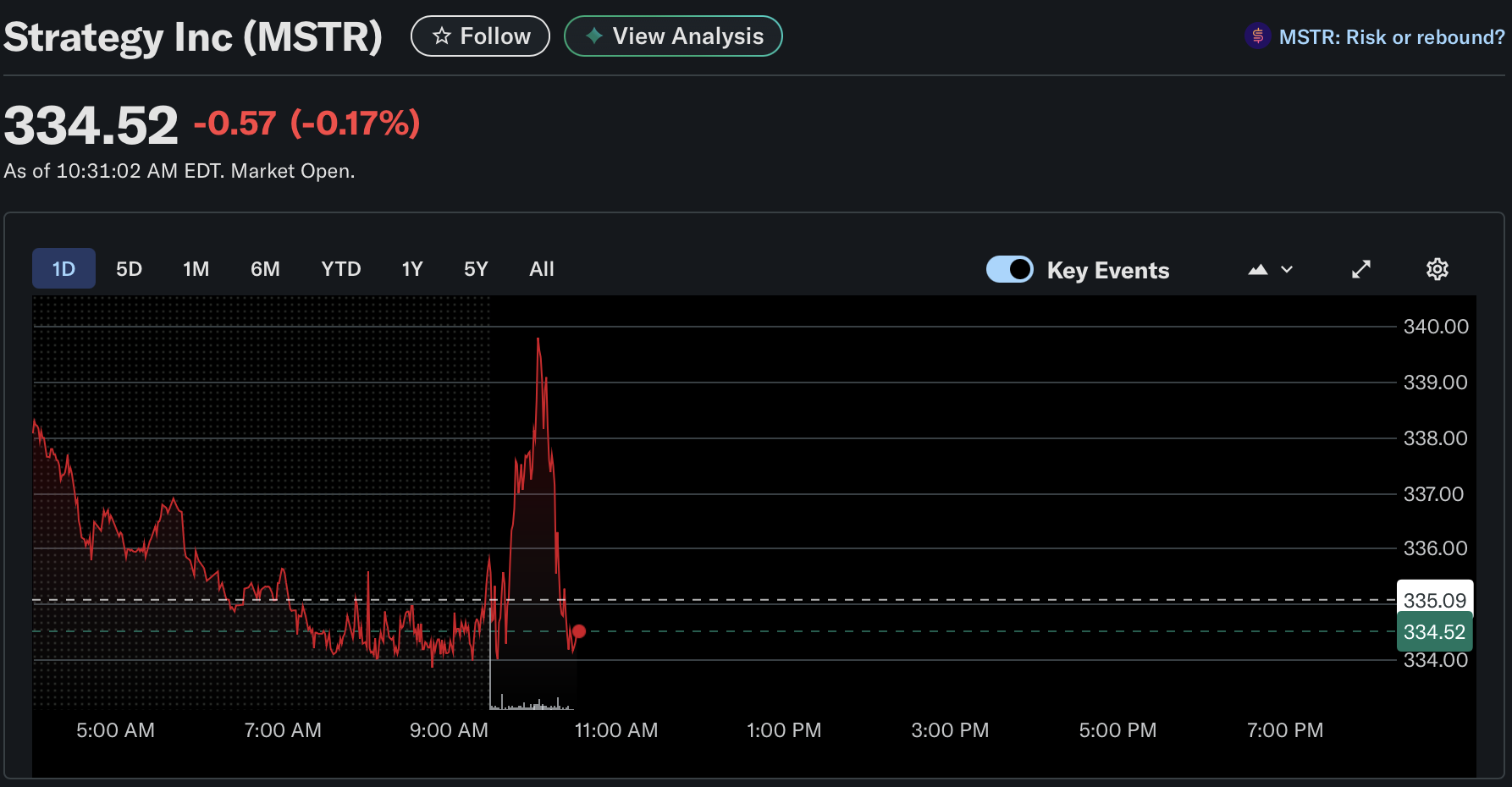

In US Wednesday’s morning session, Strategy Inc. (MSTR) traded at $334.52, marking a 0.17% decline as of 10:31 a.m. EDT. The stock initially slipped in pre-market trading, briefly spiked toward $339.50 after the open, and then pulled back below $335, highlighting the volatility that has defined recent sessions.

The intraday swings extend a broader cooling trend. Over the past five trading days, MSTR is hovering slightly in the red, and the one-month chart shows a pullback of nearly 10%. That contrasts with gains in both the finance sector (above 2%) and the S&P 500 (again above 2%), underscoring how far the stock has lagged its peers.

Still, year-to-date performance remains positive at just around 13%, reflecting the stock’s tight correlation with Bitcoin’s long-term direction. Technical traders, however, warn of caution signs: the daily chart has formed a death cross pattern, a bearish signal that often suggests prolonged weakness ahead.

Expanding Bitcoin reserves and yield

While the stock falters, the company’s Bitcoin treasury continues to grow. Chairman Michael Saylor revealed that Strategy recently added 525 BTC for $60.2 million, purchased at an average of $114,562 per coin.

That brings total holdings to 638,985 BTC, accumulated at a combined cost of $47.23 billion, with an average entry price of $73,913. With Bitcoin’s price above that level, the firm remains in profitable territory on its balance sheet.

Even more notable is the company’s internally tracked Bitcoin Yield, which measures the growth of its BTC position relative to its investment. Year-to-date, Strategy has achieved a yield of 25.9% in 2025, underscoring the effectiveness of its aggressive buying program during a period of rising Bitcoin prices.

Analyst ratings show caution

Despite the impressive Bitcoin gains, equity analysts are less convinced about the outlook for MSTR stock. Zacks currently assigns the company a Rank #4 (Sell), pointing to possible underperformance in the near term.

Earnings expectations for the current quarter call for a small loss of $0.11 per share, though that’s a major improvement compared to last year’s deep losses. Revenue is projected at $118.2 million, up just under 2% from a year ago.

The muted growth trajectory, combined with a reliance on dilution-heavy fundraising, has made some analysts wary. Monness strategist Gus Gala, for example, maintains a bearish target of $175, nearly 50% below current levels. His argument is that Strategy’s stock premium over its Bitcoin reserves has narrowed sharply and could compress further, leaving little upside to justify present valuations.

Dilution and funding methods under scrutiny

One sticking point for bears is the way Strategy finances its ongoing Bitcoin buying spree. Traditional debt markets have been less accessible on favorable terms, so the company has leaned heavily on issuing new equity. Reports suggest that about 90% of its recent fundraising has come through common stock issuance, which dilutes existing shareholders.

The latest $60 million Bitcoin purchase was backed by preferred shares rather than common stock, but analysts warn the long-term effect is similar: shareholder value gets stretched thinner with each deal. Critics argue this approach increases financial risk, particularly if Bitcoin experiences extended volatility.

Valuation pressures intensify

Another challenge lies in the company’s market multiple. Strategy once traded at a robust premium compared to the value of its Bitcoin holdings, but that advantage is shrinking. Its multiple has slipped to around 1.3x, barely above the sector median of 1.21x. Without a meaningful premium, skeptics believe the stock could remain rangebound or even drift lower.

Adding to the uncertainty, more companies have begun experimenting with Bitcoin treasury models of their own, eroding Strategy’s uniqueness. This “copycat” effect may further limit its ability to justify a rich valuation compared to peers.

What’s next for MSTR?

The disconnect between rising Bitcoin yield and falling stock performance puts investors in a difficult position. Bulls argue that as long as Bitcoin continues trending upward, Strategy’s balance sheet strength will eventually be reflected in the share price. They also point to past rallies, when the stock far outpaced Bitcoin itself.

Bears counter that dilution, shrinking premiums, and analyst downgrades make the risk/reward less attractive. If the stock continues to lag its Bitcoin exposure, investors seeking direct crypto leverage may increasingly bypass MSTR for Bitcoin itself.

As investors weigh these questions, attention has begun to spread toward other equity-linked plays that connect traditional markets with digital assets. One of the most talked-about names in this space is HYLQ Strategy Corp, which is positioning itself as a new type of crypto treasury vehicle.

HYLQ: Building a Public Treasury Around HyperLiquid

HYLQ Strategy Corp has redefined itself as “The Public HYPE Treasury,” abandoning its earlier diversification in gaming and fintech to focus exclusively on HyperLiquid’s HYPE token. The company holds nearly 29,000 tokens acquired around $37–$39 each, with current prices near $55, giving it a strong unrealized gain. Unlike many speculative crypto equities, HYLQ’s listing on the Canadian Securities Exchange (CSE) provides regulatory oversight, audited reporting, and accessible trading through platforms like Interactive Brokers.

HyperLiquid itself has grown into a leading decentralized derivatives exchange, processing between $500 million and $4 billion in daily volumes and surpassing $2 trillion in lifetime transactions. Its appeal lies in zero-gas fees, sub-second settlement speeds, and a Layer-1 blockchain capable of handling 200,000 orders per second. By holding HYPE tokens and offering a regulated equity wrapper, HYLQ gives investors a unique way to tap into DeFi’s momentum without direct exposure to wallets or on-chain risks.

Conclusion

Strategy’s story in 2025 captures the paradox of being a corporate Bitcoin heavyweight. On one hand, its aggressive accumulation strategy and 25.9% yield on BTC holdings showcase the benefits of long-term conviction. On the other hand, equity dilution, valuation compression, and bearish analyst sentiment have left its shares under pressure.

For traders and long-term holders alike, the big question is whether Strategy can realign its stock performance with its growing Bitcoin dominance, or whether the gap will widen further in coming quarters. And while Strategy dominates this debate, a quieter narrative is forming around newer players such as HYLQ Strategy Corp, which is taking a different approach by tying shareholder value to DeFi exposure through HyperLiquid. The rising attention on HYLQ serves as a reminder that the universe of crypto-linked equities is expanding, even as Strategy continues to define the category.

Fill in necessary fields and publish