Memecoins: Culture, Casinos, and Power Laws (Galaxy Report)

We may earn commissions from affiliate links or include sponsored content, clearly labeled as such. These partnerships do not influence our editorial independence or the accuracy of our reporting. By continuing to use the site you agree to our terms and conditions and privacy policy.

Memecoins sit at the intersection of culture and speculation, and they’re not going away.

According to a 2024–2025 analysis by Galaxy Research, the sector has matured and scaled even as most tokens trend to zero. Joke coins now function as on-ramps: they pull new users into wallets and DEXs who would never touch crypto otherwise. But the game is largely PvP and short-horizon, with losses concentrated among late or unlucky traders.

Pump.fun and the Supply Explosion

Per Galaxy, the January 2024 launch of Pump.fun cut the cost and complexity of token creation to almost nothing. Solana’s token count exploded to ~32 million (from <8 million pre-launch), and ~12.9 million of those came from Pump.fun alone.

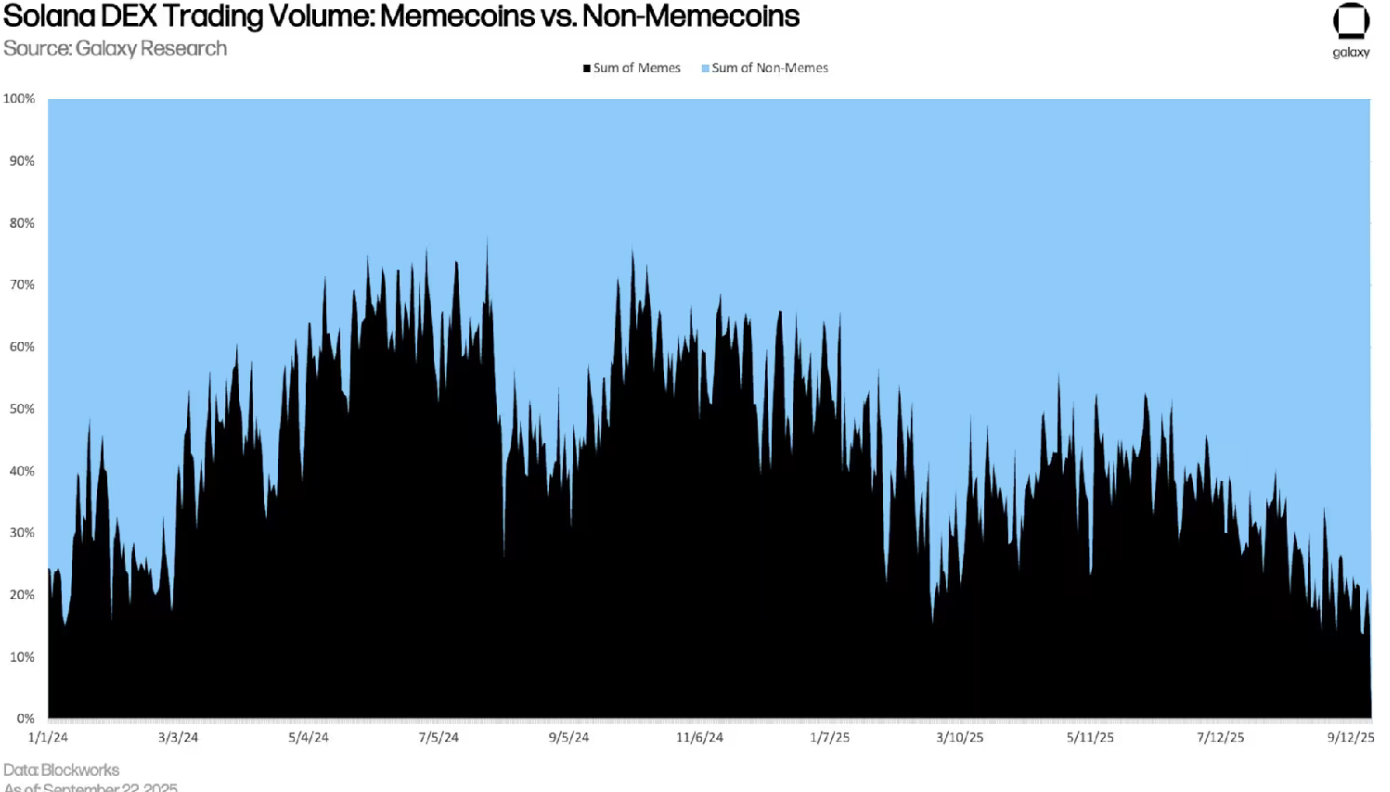

Value is just as concentrated: Pump.fun tokens hold >$4.8B FDMC, yet 12 tokens (0.00009%) capture >55% of that—classic power-law dynamics. Meanwhile, meme share of Solana DEX volume fell from ~60% in late 2024 to ~20–30%more recently as stablecoin and major-pair flows grew and on-chain perps (e.g., Hyperliquid) siphoned activity.

Hyper-Scalpy Trading Behavior

Median hold times on Solana collapsed to ~100 seconds (from ~300s a year earlier). As trade frequency rises, holds compress into the 80–120s range; only the heaviest traders hold slightly longer.

Automation (Axiom/BONKbot/Trojan), instant-fill UX, and sniper/bundler tooling reinforce the seconds-long attention cycle. According to Galaxy’s data, value accrues mainly to infrastructure, launchpads, aggregators, bots, and perps venues—rather than to most tokens.

Chains and Venues Specialize

Solana dominates new launches (low fees, high throughput, strong “degen” culture). BNB Smart Chain leads large swaths of spot meme volume (four.meme, AsterDEX catalysts). Ethereum hosts legacy memes (DOGE, PEPE, MOG, SPX6900) with longer half-lives, while Base carves out niches in AI/SocialFi (e.g., Zora).

Galaxy also notes Base is building a bridge to Solana, potentially easing liquidity flow between ecosystems.

Launchpads: Winner-Takes-Most

Pump.fun briefly ceded share to Bonk.fun over summer but reasserted dominance, per Galaxy. Even celebrity tokens (e.g., $YZY, $TRUMP) sometimes bypass launchpads entirely, using Meteora for bespoke liquidity control to mitigate early bot capture.

Risks in the Meme Economy

Galaxy details persistent honeypots, rug liquidity pulls, and vampire “vamping” where copycat tokens overtake originals via coordinated KOL shilling. Median hold times and concentration stats underscore negative expected value for most traders. Regulatory risk lingers, as headline scandals can prompt clampdowns.

Creator Capital Markets

Galaxy highlights Pump.fun’s Project Ascend, which routes a sliding share of trading fees to creators (higher at small caps, lower at scale), plus the rise of stream-tied token launches. The model aligns attention with liquidity, but longevity is unproven.

Bottom Line

Memecoins now represent tens of millions of tokens and billions in FDMC, yet outcomes are governed by power laws: a microscopic minority captures most value. The sector’s significance lies less in “utility” and more in the infrastructure, culture, and onboarding it fuels, even as most participants face a negative-EV, seconds-long trading arena.

Fill in necessary fields and publish