From Mobile Apps to On-Chain Finance: The Neobank Expansion Story

We may earn commissions from affiliate links or include sponsored content, clearly labeled as such. These partnerships do not influence our editorial independence or the accuracy of our reporting. By continuing to use the site you agree to our terms and conditions and privacy policy.

The scale of change underway in digital banking is no longer theoretical - it’s showing up clearly in the data.

What started as app-based alternatives to traditional banks is rapidly transforming into something much larger: a borderless financial layer built on software and, increasingly, blockchain infrastructure.

Recent market projections illustrate just how dramatic this transition could become over the next decade.

A Growth Curve That’s Steepening, Not Flattening

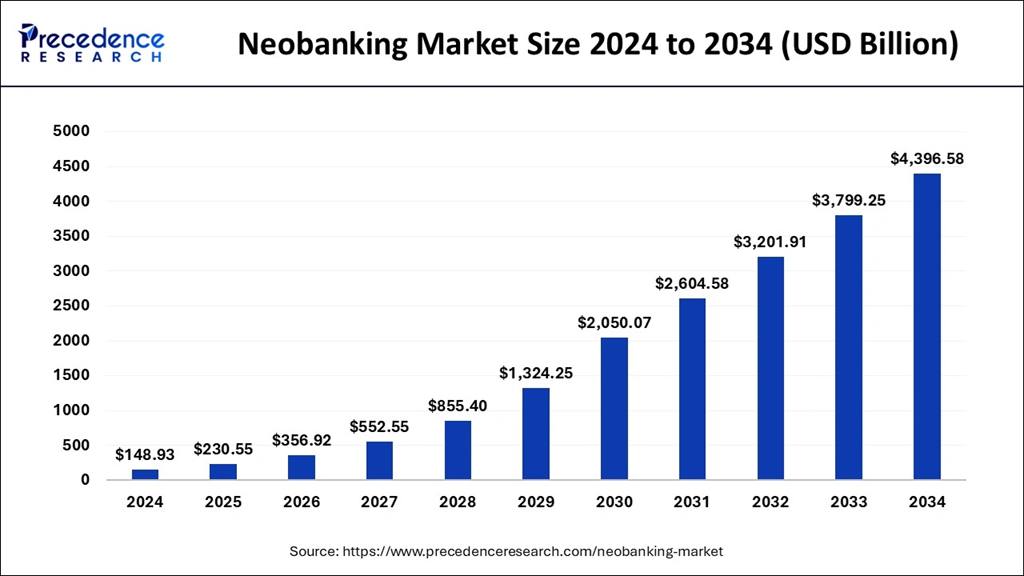

Current estimates place the global neobanking market at just under $150 billion in 2024. That figure alone is notable, but what follows is more revealing. Forecasts show the sector crossing the $1 trillion mark before the end of the decade and continuing to expand aggressively into the early 2030s, with total market value potentially exceeding $4 trillion.

This isn’t the kind of growth associated with mature industries. The curve steepens as time progresses, meaning each year adds more absolute value than the last. That pattern typically appears when a technology shifts from early adoption into mainstream usage – not when it is nearing saturation.

In other words, the market is signaling that neobanking is still in the early chapters of its expansion.

The Shift From “Digital Banks” to On-Chain Finance

What separates the next generation of neobanks from earlier versions is architecture. Many first-wave neobanks still depended heavily on traditional banking partners, custodians, and regional payment systems. Newer, crypto-native platforms operate very differently.

On-chain neobanks run core financial functions directly on blockchain networks. Balances, transfers, and settlement occur transparently and continuously, without relying on legacy clearing systems. This approach eliminates many of the structural bottlenecks that slow down traditional finance.

As a result, these platforms can manage large pools of assets without physical branches, without correspondent banks, and without the geographic constraints that have historically defined financial institutions.

Always-On, Borderless by Design

One of the most important implications of this model is operational speed. On-chain systems do not shut down for weekends, holidays, or regional business hours. Transactions can settle globally in real time, regardless of where users are located.

This “always-on” architecture also changes how these platforms scale. Growth no longer depends on opening new locations or building local infrastructure. Software updates and smart contracts replace expansion through brick-and-mortar operations, allowing neobanks to grow at a pace traditional institutions cannot easily match.

What the Projections Really Suggest

The multi-trillion-dollar projections aren’t just about more users opening digital accounts. They reflect expectations that neobanks – particularly on-chain ones – will take on a broader role across payments, savings, asset management, and cross-border money movement.

If those forecasts prove accurate, the implication is clear: financial services are shifting from nationally segmented systems toward global, software-driven networks. In that environment, neobanks are not niche alternatives – they become foundational infrastructure.

The takeaway from the data is straightforward. The neobanking sector isn’t merely growing; it’s undergoing a structural expansion that could redefine how financial services are delivered worldwide. And based on the trajectory, this transformation appears to be accelerating, not slowing down.

Fill in necessary fields and publish