Bitcoin’s Active Addresses Drop Sharply as ETFs Reshape Market Cycle

We may earn commissions from affiliate links or include sponsored content, clearly labeled as such. These partnerships do not influence our editorial independence or the accuracy of our reporting. By continuing to use the site you agree to our terms and conditions and privacy policy.

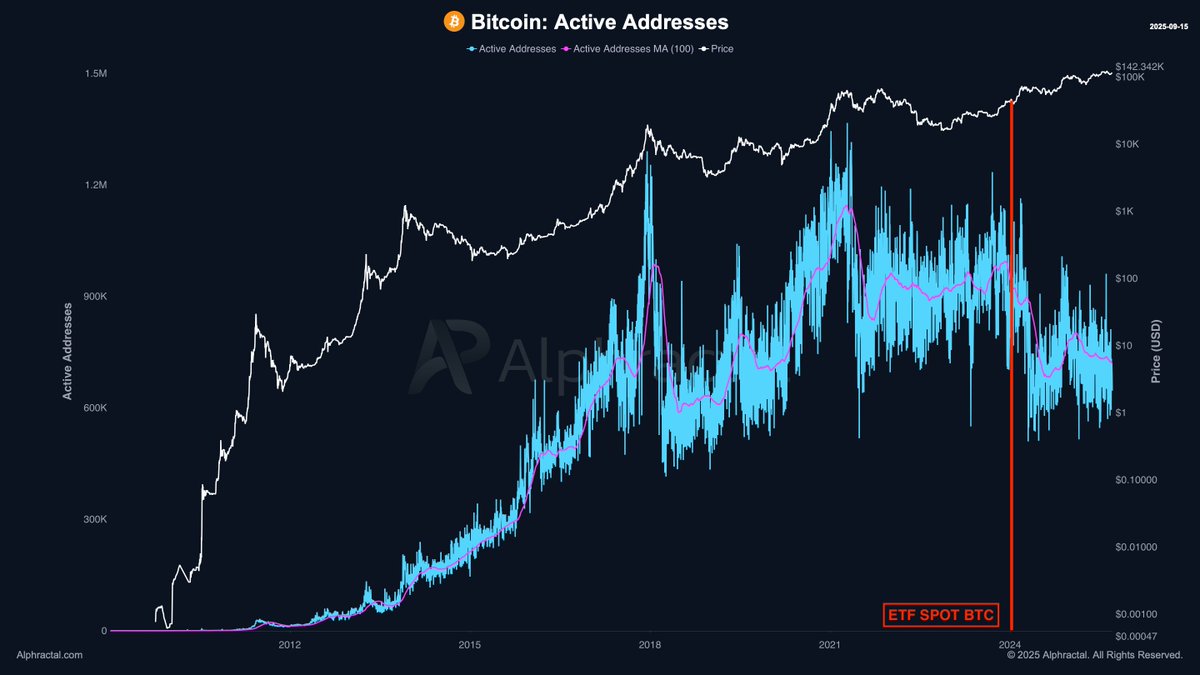

Bitcoin is showing signs that this market cycle may not mirror the patterns of previous ones. While price remains in line with long-term historical trends, fresh data on network activity paints a different picture of what’s driving demand in 2025.

Active addresses decline despite rising prices

One of the most striking shifts is the fall in active addresses. Historically, these surged during bull markets as retail investors rushed on-chain. This time, however, activity has been trending down steadily since 2021, even as Bitcoin climbed to fresh all-time highs above $140,000.

Charts from Alphapractal confirm that current address counts remain well below previous peaks. This suggests that Bitcoin’s growth is increasingly being fueled off-chain rather than through direct wallet activity.

ETFs and centralized platforms change investor behavior

Analysts argue that the launch of spot Bitcoin ETFs in 2024 played a major role in this divergence. The new funds allow institutions and retail investors to gain exposure without opening wallets, moving coins, or worrying about custody.

Centralized exchanges (CeXs) have also lured investors with yield products tied to BTC holdings. By keeping assets parked on these platforms, participants bypass traditional on-chain interactions, suppressing address metrics.

Long-term holders add another layer

Another factor is dormant wallets. Many long-term holders continue to sit on their coins without moving them, further reducing the number of active addresses tracked each day.

This evolution signals that Bitcoin demand may be increasingly shaped by financial products and passive holding strategies rather than grassroots transaction activity.

A new cycle dynamic?

Together, these shifts highlight why this cycle could unfold differently from the past. Bitcoin remains aligned with its broad cyclical trajectory, but the mechanics underneath have changed. Investor demand is increasingly mediated through ETFs, custodians, and CeX products rather than direct blockchain engagement.

That raises an important question: if on-chain activity is no longer the dominant signal of demand, how should markets measure the strength of this cycle? For now, the answer seems clear, price action may still follow the cycle, but the drivers are evolving rapidly.

Fill in necessary fields and publish