Ethereum Wallet Growth Outpaces Bitcoin Amid Stablecoin Surge

04.09.2024 20:30 1 min. read Alexander Stefanov

Ethereum wallet adoption is accelerating, outpacing Bitcoin in growth due to its broader functionality beyond just holding cryptocurrency.

While Bitcoin wallet creation has slowed, Ethereum wallets are on the rise, growing by 2% in the past month to 281.7 million. This increase is largely driven by Ethereum’s role in accessing decentralized applications (dApps) and its use in stablecoin transactions, particularly Tether (USDT).

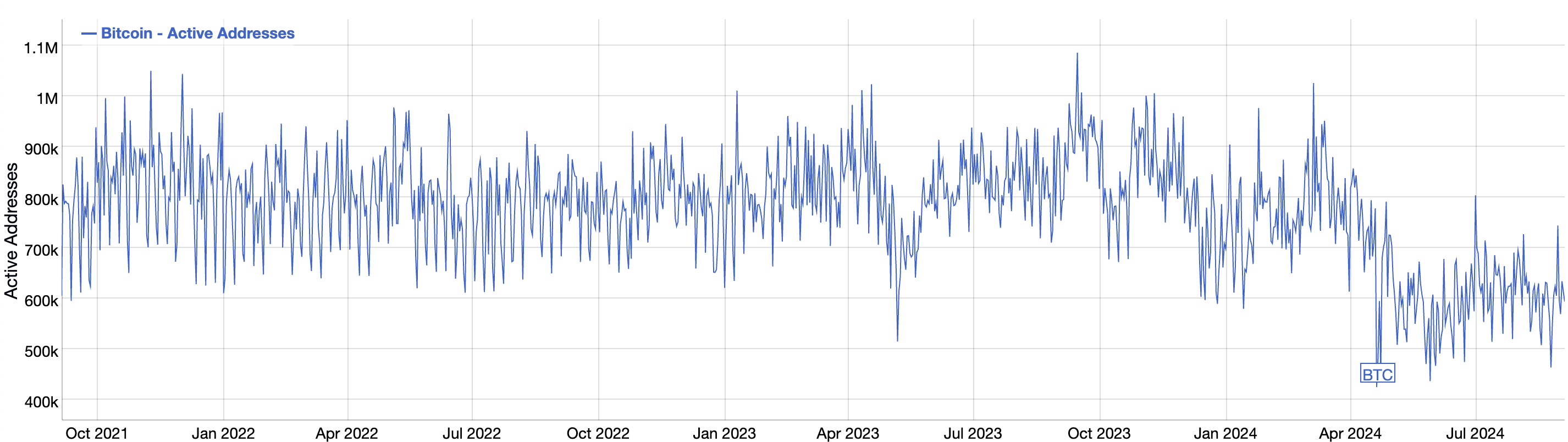

Bitcoin, meanwhile, has seen only a 1% increase in wallets with non-zero balances, reaching 54.1 million. The network’s activity has declined, with fewer daily active addresses and a drop in retail engagement, especially as interest in features like Ordinals and Runes fades.

Ethereum’s wallet growth is also tied to the increasing popularity of stablecoins. Tether, in particular, has seen a rise in users, with more wallets holding USDT as it remains a key source of liquidity in the market.

Despite this, Ethereum’s price continues to face downward pressure, with predictions of further declines before any potential recovery.

At the same time, Ethereum’s role as the backbone for Layer 2 solutions remains strong, with significant funds flowing between Ethereum and these scaling networks. This ongoing activity highlights Ethereum’s central position in the crypto ecosystem, even amid market volatility.

-

1

Ethereum Tops $3,285 for First Time Since January

17.07.2025 7:00 1 min. read -

2

XRP Hits All-time High Amid Regulatory Breakthrough and Whale Surge

18.07.2025 11:14 2 min. read -

3

Trump’s Truth Social to Launch Utility Token for Subscribers

10.07.2025 18:30 1 min. read -

4

Grayscale Reveals Which Altcoins Are Next in Line for Onclusion

11.07.2025 10:00 1 min. read -

5

Arthur Hayes Predicts Monster Altcoin Season: Here is Why

12.07.2025 10:46 1 min. read

Fartcoin Price Prediction: Trader Expects Big Bounce as FARTCOIN Nears $1

Fartcoin (FARTCOIN) has gone down by 17.3% in the past 24 hours and currently sits at $1.14. As the token approaches $1, one trader favors a bullish Fartcoin price prediction. DevKhabib, a pseudonymous trader whose X account is followed by nearly 46,000 users, says that he expects a big bounce off the $1 support after […]

Whale Activity Spikes as Smart Money Eyes Reversal Zones

Amid current market volatility, blockchain analytics firm Santiment has reported a notable rise in whale activity targeting a select group of altcoins.

Binance to Launch PlaysOut (PLAY) Trading on July 31 With Airdrop

Binance has officially announced the launch of PlaysOut (PLAY), a new token debuting on Binance Alpha, with trading scheduled to begin on July 31, 2025, at 08:00 UTC.

Cboe BZX Files for Injective-based ETF Alongside Solana Fund Proposal

The Cboe BZX Exchange has submitted a filing with the U.S. Securities and Exchange Commission (SEC) seeking approval for a new exchange-traded fund (ETF) that would track Injective’s native token (INJ).

-

1

Ethereum Tops $3,285 for First Time Since January

17.07.2025 7:00 1 min. read -

2

XRP Hits All-time High Amid Regulatory Breakthrough and Whale Surge

18.07.2025 11:14 2 min. read -

3

Trump’s Truth Social to Launch Utility Token for Subscribers

10.07.2025 18:30 1 min. read -

4

Grayscale Reveals Which Altcoins Are Next in Line for Onclusion

11.07.2025 10:00 1 min. read -

5

Arthur Hayes Predicts Monster Altcoin Season: Here is Why

12.07.2025 10:46 1 min. read