Ethereum Wallet Growth Outpaces Bitcoin Amid Stablecoin Surge

We may earn commissions from affiliate links or include sponsored content, clearly labeled as such. These partnerships do not influence our editorial independence or the accuracy of our reporting. By continuing to use the site you agree to our terms and conditions and privacy policy.

Ethereum wallet adoption is accelerating, outpacing Bitcoin in growth due to its broader functionality beyond just holding cryptocurrency.

While Bitcoin wallet creation has slowed, Ethereum wallets are on the rise, growing by 2% in the past month to 281.7 million. This increase is largely driven by Ethereum’s role in accessing decentralized applications (dApps) and its use in stablecoin transactions, particularly Tether (USDT).

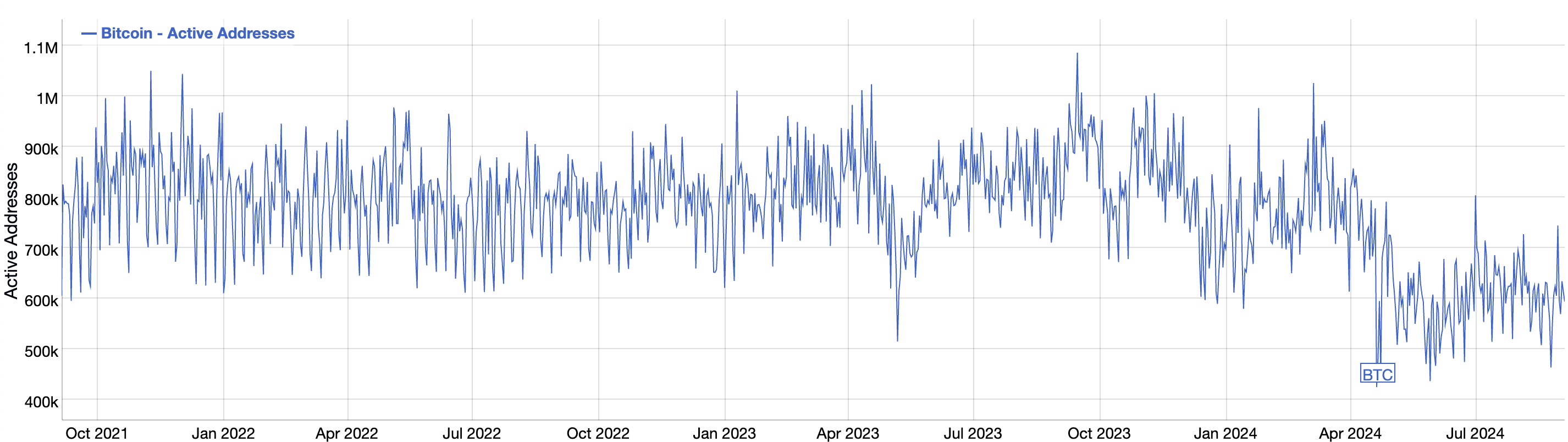

Bitcoin, meanwhile, has seen only a 1% increase in wallets with non-zero balances, reaching 54.1 million. The network’s activity has declined, with fewer daily active addresses and a drop in retail engagement, especially as interest in features like Ordinals and Runes fades.

Ethereum’s wallet growth is also tied to the increasing popularity of stablecoins. Tether, in particular, has seen a rise in users, with more wallets holding USDT as it remains a key source of liquidity in the market.

Read More:

Despite this, Ethereum’s price continues to face downward pressure, with predictions of further declines before any potential recovery.

At the same time, Ethereum’s role as the backbone for Layer 2 solutions remains strong, with significant funds flowing between Ethereum and these scaling networks. This ongoing activity highlights Ethereum’s central position in the crypto ecosystem, even amid market volatility.

Fill in necessary fields and publish